Getting ready for retirement often means collecting pieces of information from multiple agencies so that you can begin to envision your life post-retirement. This is part 2 of a 3-part series:

Part 1: Gathering estimates for your health care premium

Part 2: Where will your monthly income come from?

Part 3: What can you do right now?

How much will retirement cost me?

You’ve begun finding out in Part 1 how much your retirement will cost. Most financial planners agree that the average individual will need between 70% and 90% of his or her pre-retirement income to live comfortably. You will have to anticipate your own income needs, which will include inflation. For the last 25 years, inflation has averaged 2.76% (Source).

Not only will inflation affect your future household income, but it will also affect your purchasing power. Let’s assume that you have $10,000 today and there will be an average of 4% inflation in the coming years. That money will be worth $6,756 in 10 years, $4,564 in 20 years, and $3,083 in 30 years if it is not earning any interest.

Also consider your anticipated retirement age and the longevity of your life. Thanks to modern medicine and other breakthroughs, life expectancy has risen through the years. According to data compiled by the Social Security Administration, a man turning 65 today can live (on average) until age 84. Women can expect to live until 86. Are you curious to know how long an individual of your generation might live? Here’s a convenientlife-expectancy calculator to plan for the average numbers of years a person can expect.

What are your sources of income?

Most people realize that no one source will provide all their income in retirement. Diversifying your income is one way you can plan to meet the needs of a longer, more active retirement.

Your sources of income may include:

- Social Security

- MOSERS

- Personal savings and/or investments

- Re-employment

MOSERS provides all members an annual, personalized benefit statement that will project a pension benefit based on your salary, service history, and a retirement multiplier. If you have not yet received it, you may find it on our Secure Site under Estimates.

The Social Security Administration provides both a Quick Retirement Calculator, a Retirement Estimator, as well as your official social security statement online. In order to access your online statement, you will have to create an account with a valid email address, social security number, and US mailing address.

Your personal savings and investments may come from a number of sources. If you were hired after June 1, 2012, you were automatically enrolled into Missouri’s Deferred Compensation plan (check your balance here) You may also have savings and investments from other plans, such as previous employers or your own IRA.

Re-employment is another option. Many view their retirement as a chance to pursue another career dream. Your MOSERS benefit will not be affected by full-time employment unless you begin working at a MOSERS benefit-eligible position with the state of Missouri.

Putting it together:

Let’s use some real numbers for a bit and look at an average retiree if he or she were retiring this month under the MSEP 2000:

- $2,500 monthly Final Average Pay

- Will retire at age 62

- 23 years of credited service at retirement.

- 1.7 (0.017) multiplier for MSEP 2000*

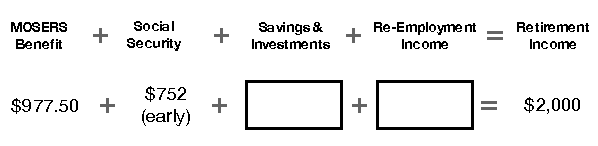

Using the estimate that an individual will need roughly 80% of his or her income during retirement, we can determine that the member will need $24,000 a year or $2,000 per month. Using the MOSERS Retirement Benefit Estimate Formula, we’ve found out that his or her retirement benefit will be $977.50 a month.

As you can see, our example member will need an additional $1022.50 a month to meet his post-retirement income goal. Social security can help fill that gap, but that amount varies depending on when the member chooses to start receiving that benefit. You may start drawing social security at age 62, but at a reduced rate. For convenience, we’ve included an early retirement social security estimate below:

You will have to determine your own individual sources of income, but we recognize that it might be difficult to navigate each website. We recommend that state employees use MO Deferred Comp’s RetiremenTrack tool, which is specifically designed for state of Missouri employees. Simply enter your income, pension, and savings information and the calculator will reveal if you’re on track for your retirement goals.

*If you would like to complete your own formula, please use the following multipliers:

MSEP = 1.6% (0.016) MSEP 2011 = 1.7% (0.017)